OBBBA Breakdown: What High-Income Taxpayers Need to Know About Itemized Deductions

For nearly a decade, most high-income taxpayers didn’t have to think much about itemized deduction limitations. After the Tax Cuts and Jobs Act, many of the old phaseouts were effectively sidelined, and planning conversations shifted elsewhere.

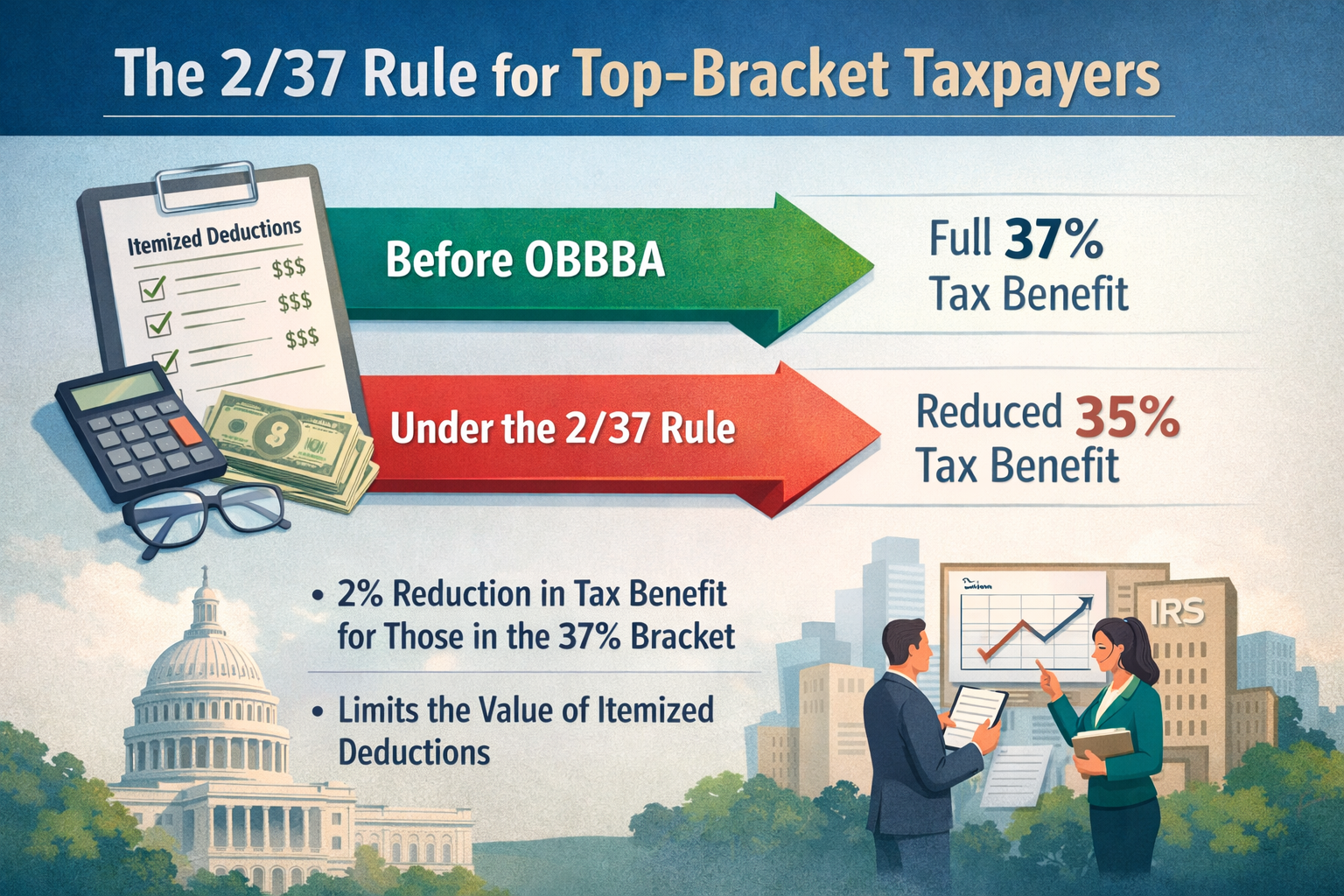

Under the recently enacted One Big Beautiful Bill Act (OBBBA), a new limitation applies to itemized deductions for taxpayers in the top marginal tax bracket. This provision—often referred to as the “2/37 rule” under Section 70111—doesn’t eliminate deductions outright, but it does reduce their tax value in a way that can meaningfully affect high-income households.

In this post, we’ll explain how the rule works, who it affects, and why it matters for tax planning going forward.

A Quick Refresher: Itemized Deduction Limitations

Historically, Congress has periodically limited itemized deductions for higher-income taxpayers. These rules were designed to reduce the tax benefit of deductions as income increased, rather than disallowing deductions entirely.

The key point is that limitation regimes typically affect the value of deductions, not whether they exist. You may still be allowed to deduct an expense, but the tax savings associated with that deduction may be less than your marginal tax rate would suggest.

After the TCJA, many of these limits were suspended or became irrelevant for most taxpayers. The OBBBA brings a version of this concept back—narrowly targeted at those in the highest tax bracket.

What the OBBBA Changed

The OBBBA introduced a new limitation on itemized deductions that applies once a taxpayer reaches the top 37% marginal bracket. The rule is codified under Section 70111 and is designed to cap the effective tax benefit of certain itemized deductions.

Importantly, this provision does not apply across the board. Taxpayers below the top bracket are generally unaffected. For those above it, however, the math around deductions changes in subtle but important ways.

The “2/37 Rule” Explained

The so-called 2/37 rule gets its name from the mechanics of the limitation.

In simple terms, once a taxpayer is in the 37% bracket, the tax benefit of affected itemized deductions is reduced by 2 percentage points. Instead of receiving a full 37% tax benefit, the effective benefit is capped at 35%.

This is not a dollar-for-dollar reduction in deductions. The deduction itself still exists. What changes is the rate at which that deduction reduces tax liability.

Think of it as a reduction in the marginal value of deductions once income reaches the top bracket.

A Real World Example

Consider a married couple with income well into the 37% bracket who itemize their deductions. Assume they have $100,000 of deductible expenses that are subject to the limitation.

Before the OBBBA rule, those deductions would reduce federal tax liability by approximately $37,000.

Under the 2/37 rule, the same $100,000 of deductions now produces a tax benefit of about $35,000 instead.

Nothing about the deduction itself changed. What changed is the effective rate applied to it. For households with large deductions—particularly charitable contributions—this difference can compound over time.

Why High Earners are Most Affected

The impact of the 2/37 rule is most noticeable for taxpayers who combine very high income with significant itemized deductions. This often includes households with large charitable contributions, business owners with uneven income patterns, and taxpayers who continue to itemize despite SALT limitations.

Because the rule operates quietly in the background, many affected taxpayers may not notice its impact until they review projections or compare outcomes to prior years.

Planning Implications for High-Income Taxpayers

The return of an itemized deduction limitation doesn’t invalidate existing planning strategies, but it does change the assumptions behind them.

Charitable giving remains an important planning tool, but the expectation of a full 37% tax benefit may no longer be accurate for top-bracket income. Timing decisions—such as bunching deductions or accelerating income—should be evaluated with the reduced marginal benefit in mind.

This is also a reminder that effective tax planning is about modeling outcomes, not just maximizing individual deductions in isolation. Small changes in marginal benefit can meaningfully affect overall results at higher income levels.

Looking Ahead

In our next post, we will explore how the OBBBA affects taxes for retirees, with a closer look at planning strategies that may help mitigate its impact.

If you have questions about how the One Big Beautiful Bill Act impacts your tax situation, schedule a time with Niko Finnigan, Partner at Delta Wealth Advisors.