OBBB Breakdown: Itemized Deductions

In our first blog on the One Big Beautiful Bill Act (OBBB), we wrote about changes to tax brackets and the standard deduction. With the passage of OBBB, the attractiveness of itemizing has returned. After the 2017 Tax Cuts and Jobs Act, only 1 out of 10 tax filers itemized deductions. With the doubling of the standard deduction and changes in the 2017 tax bill, it was often smarter to use the new, larger standard deduction.

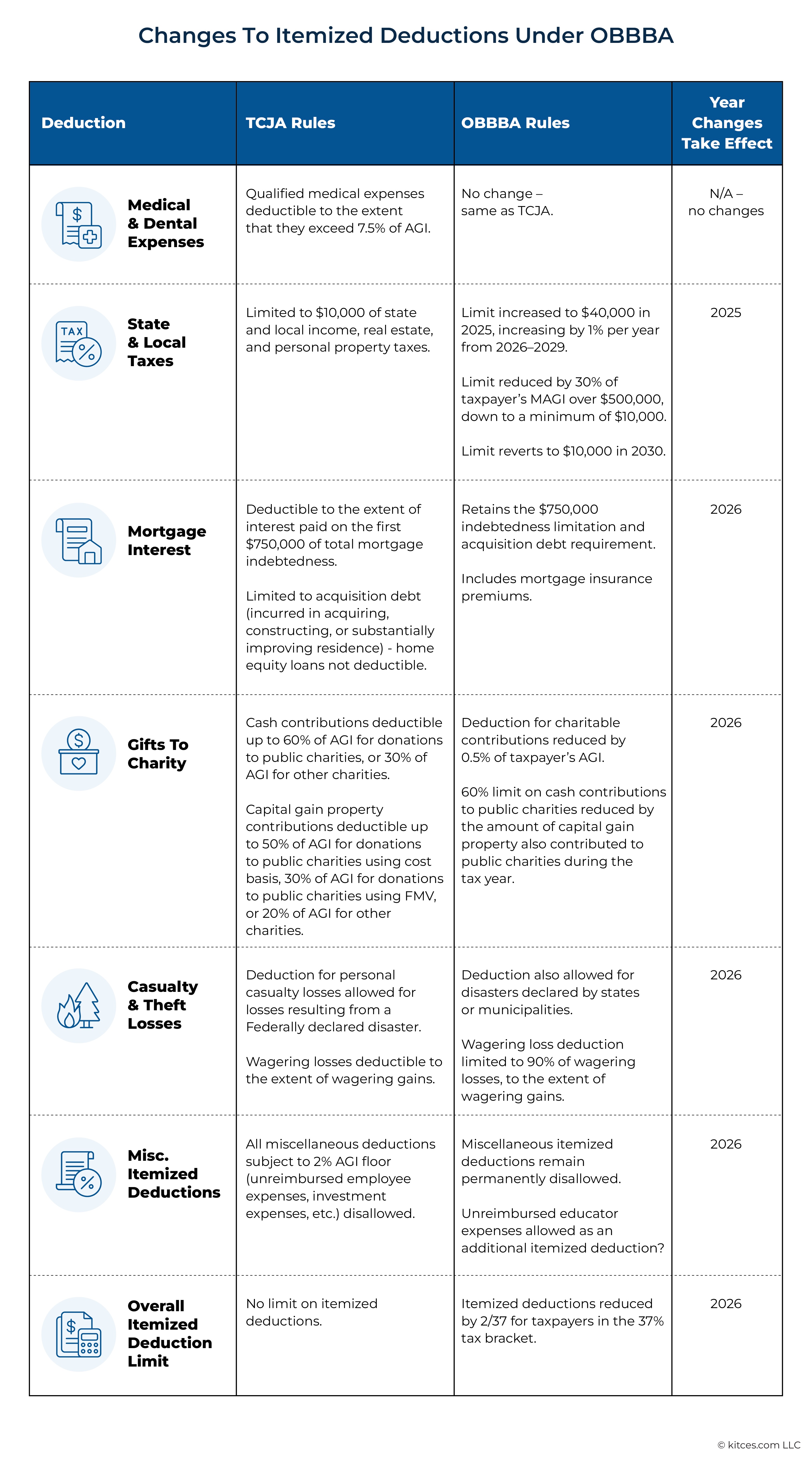

Now, some of the largest changes to the tax code made by the One Big Beautiful Bill Act (OBBB) applied to itemized deductions for tax filers. Some of these changes have phases of deductibility, while others are permanent. In our blog, we will highlight the changes to itemized deductions for State and Local Taxes (SALT), mortgage insurance, loss deductions, miscellaneous itemized deductions, and limited deductions for the 37% tax bracket.

Please note that these changes are very detailed. We've tried our hardest to make this a straightforward read, but we have to highlight the specifics of each change.

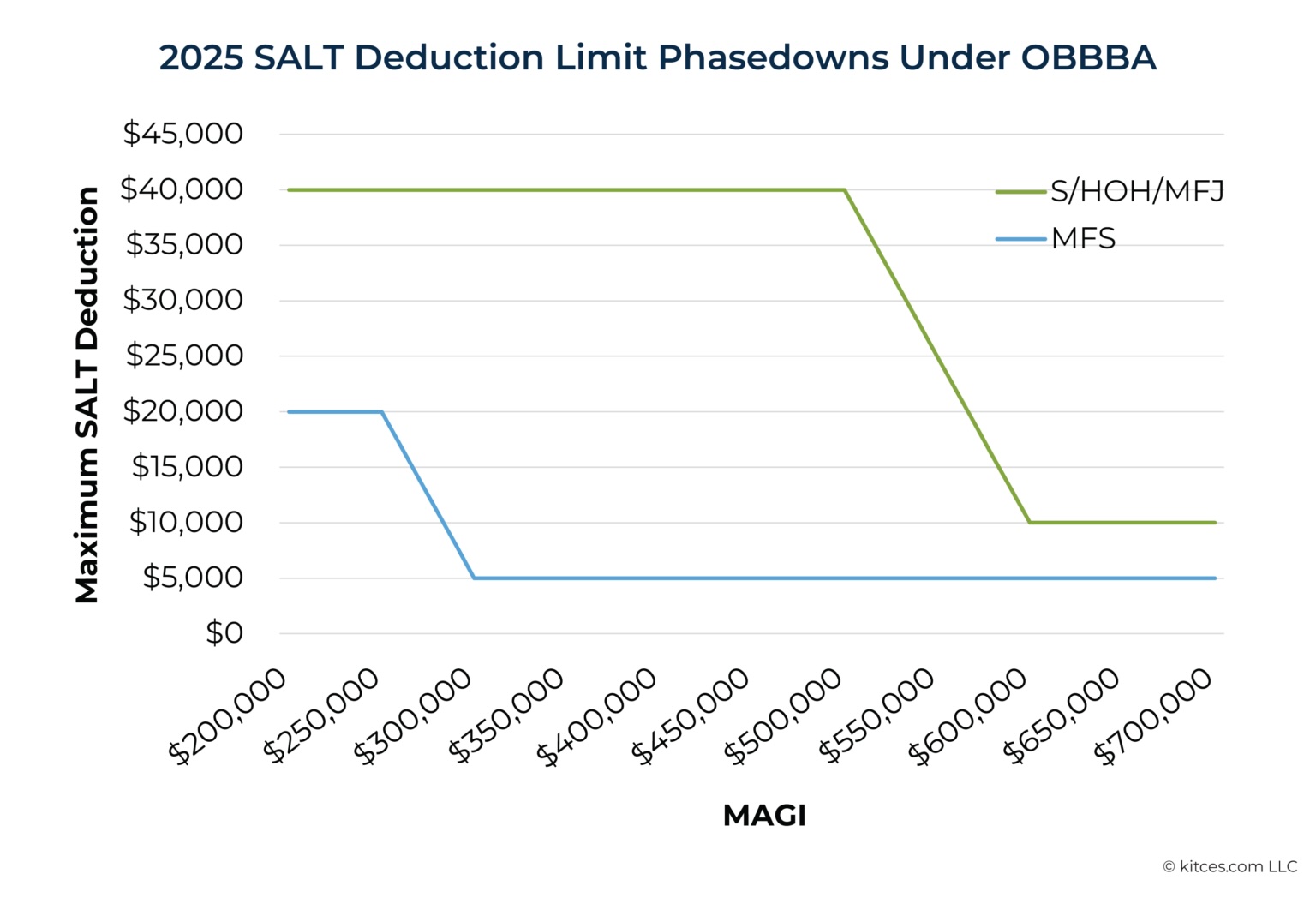

State and Local Tax Deduction

Prior to the 2017 Tax Cut and Jobs Act, state and local taxes (SALT) were entirely deductible against federal taxable income. These SALT taxes included state income tax, property taxes and local income taxes (where applicable). After the passing of the 2017 tax bill, both single and married filing jointly filers could deduct $10,000 against their federal income taxes.

With the passage of OBBB, tax filers can deduct up to $40,000 against their federal income taxes, starting in 2025. This $40k limit will be adjusted up 1% per year through 2029, with the $40k cap reverting to $10k in tax year 2030.

Planning Idea: Single and head of household filers can take advantage of the fact that the $40k cap is for all tax filers. Most deductions and limitations are 50% for single filers, but this SALT deduction is the same for single, head of household and married filing jointly taxpayers.

The SALT deduction has a caveat for high income earners. The OBBB phases down for taxpayers with a Modified Adjusted Gross Income (MAGI) over $500,000. For most taxpayers with a MAGI over $600k, the SALT deduction cap reverts to $10,000 for 2025 - 2029.

Planning Idea: Certain professions, like real estate and sales, can have lumpy income streams. If your income oscillates around $400k - $700k, your family could benefit from timing state and local taxes to years where your MAGI is lower than usual.

Mortgages

Starting with the 2017 tax bill, taxpayers cannot deduct primary home mortgage interest above the first $750,000 in debt. Starting in 2022, home owners were not allowed to deduct mortgage insurance (PMI) against their federal income taxes. The OBBB allows for home owners to deduct PMI against their federal income taxes starting in tax year 2026.

Charitable Deductions

Prior to the OBBB, the government had imposed ceilings on the max deductibility of contributions to public and private charities. With the passage of the OBBB, there is now a floor on the deductibility of charitable contributions. Starting in 2026, charitable contributions are only deductible after the taxpayers first 0.5% of Adjusted Gross Income (AGI).

For example, if a couple has an AGI of $300,000 and makes total cash contributions of $10,000 to public charities, the couple will only be able to deduct $8,500 against their federal taxable income.

Planning Idea: For charitably inclined families, the importance of donation bunching is even greater than before. 2025 tax year is not subject to the 0.5% floor, making it attractive to pull forward 2026 donations into 2025. Starting in 2026, if charitable contributions exceed the ceiling limit for each tax year, the excess is carried forward into future years. This is a way to plan around the 0.5% floor.

Please note that the OBBB does contain new below the line deductions for charitable contributions. We will discuss in a future blog.

Loss Limitations

Starting in 2026, gamblers will only be able to deduct 90% of their losses against their winnings. (Don't worry, that bet on the Bears to win it all will hit one year).

Also starting next year, taxpayers with losses not covered by insurance and more than 10% of their AGI from state declared disasters can deduct these expenses. Previously, only expenses from federally declared natural disasters could be deducted.

Top Income Tax Bracket Deduction Limitations

Starting in 2026, tax payers in the highest tax bracket of 37% federally are subject to new itemized deduction limitations. This new limitation reduces itemized deductions by 2/37th for the lesser of 1.) taxpayer's total itemized deductions or 2.) the taxpayers taxable income plus itemized deductions that exceed the 37% tax bracket.

In plain English, for most high income earners who itemize on their tax return, this means roughly 5% of the itemized deductions will not be recognized on the tax return.

Critically, section 70111 of the OBBB, which applies this rule, specifically mentions that the 2/37 rule will not apply to the Qualified Business Income calculation. (We will expand upon the Qualified Business Income taxation in a future blog.)

Planning Idea: For taxpayers in the highest tax bracket, effectively 5% of deductions lose their value starting in tax year 2026. These taxpayers should look to plan around making additional deductions in 2025.

In our next post, we will discuss the return of bonus depreciation. If you have specific questions on how the new tax bill impacts your financial or tax situation, please click here to schedule a time with Niko Finnigan, partner at Delta Wealth.