OBBB Breakdown: Changes to Standard Deduction

At more than 900 pages, the One Big Beautiful Bill Act (OBBB) is a monster to read and even more challenging to comprehend. To help our clients understand the impact of the new tax legislation, we are writing a series of blogs to digest the OBBB. Each blog will be short and focused on a specific topic within the OBBB.

One of the most common questions we get about the OBBB is "How will this affect the tax brackets and standard deduction?"

Tax Bracket Updates

Tax brackets changed significantly from 2016 to 2017. Current tax brackets were set to sunset in 2026, reverting to the prior 2016 tax brackets.

The OBBB permanently extends the 2017 tax brackets into future. The 10% and 12% tax brackets also adjusted minimally upward by less than $1,000 in each tax bracket. The tax brackets for 22%, 24%, 32% and 37% remain unchanged.

Standard Deduction--What Changed?

Starting with the 2017 Tax Cut and Jobs Act, the standard deduction rose dramatically. For married filing jointly filers, the standard deduction rose from $12,700 in 2017 to $24,000 in 2018. Tied to inflation, this deduction has risen to $30,000 for married filing jointly filers in 2025.

Under the OBBB, the standard deduction rises in tax year 2025 to $31,500 for married filing jointly (MFJ) and $15,750 for single filers. These amounts will be adjusted for inflation going forward and are permanent in the tax code.

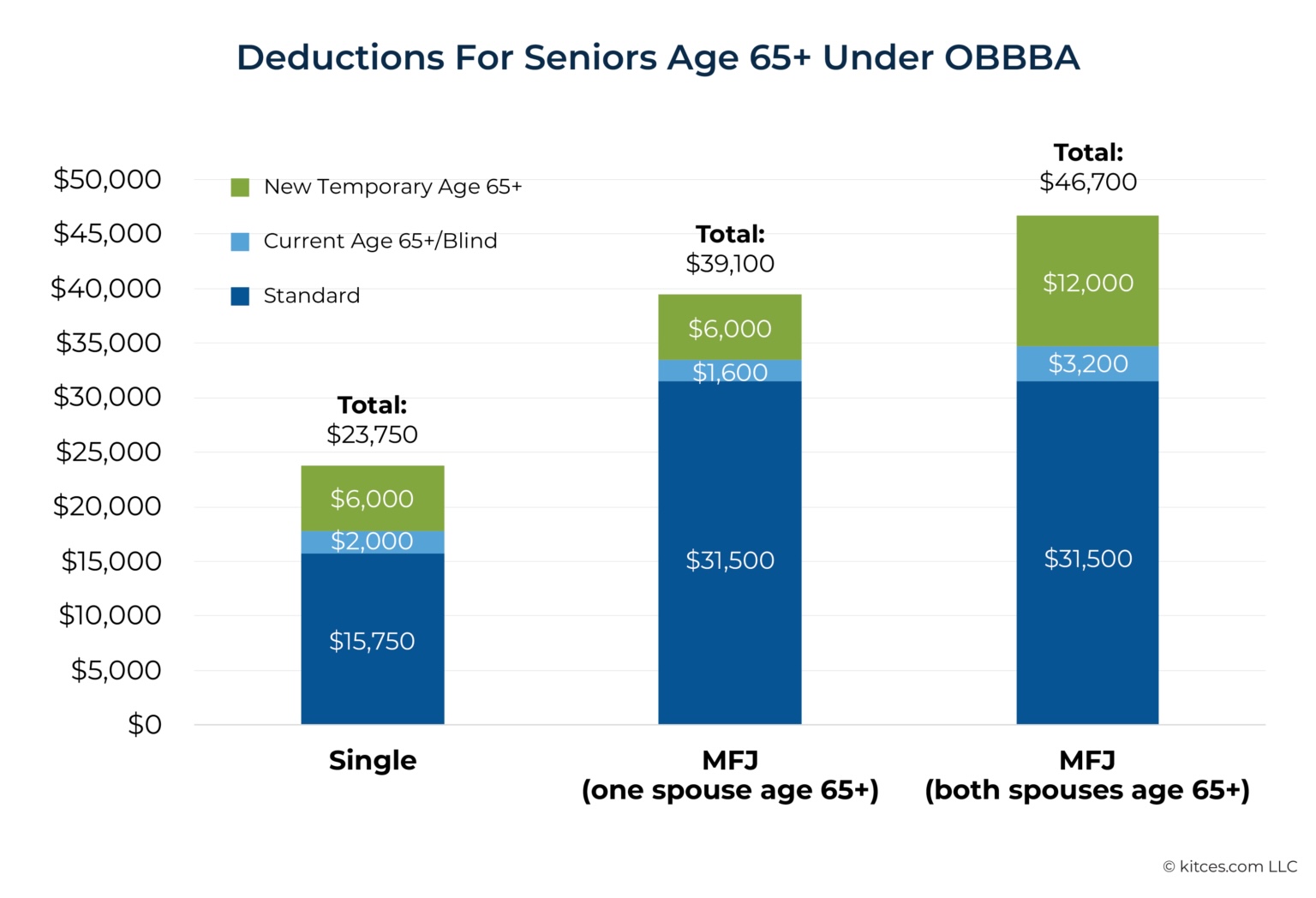

Changes to Standard Deductions for Seniors

The OBBB has some major, temporary changes for seniors (age 65 or older) starting in tax year 2025. First, all seniors receive an additional $3,200 deduction for MFJ filers.

In addition to the senior deduction, there is a temporary deduction for tax years 2025 through 2028. This $12,000 deduction for MFJ filers over 65 phases out as Modified Adjusted Gross Income exceeds $150,000. Once Modified Adjusted Gross Income exceeds $250,000 for joint filers, the $12,000 additional deduction is completely phased out.

Planning Idea: Because the additional senior deduction is temporary, this may present an opportunity to convert additional dollars from pre-tax IRA to post-tax Roth IRA's. Alternatively, clients may want to consider whether realizing capital gains in these years lowers lifetime taxes.

The Social Security Administration estimates that nearly 90% of Social Security recipients will have deductions that exceed their Social Security income. This does not mean that Social Security is tax free, as the deductions can be used against all ordinary income and regardless of whether a tax payer has opted to receive Social Security benefits.

In our next post, we will discuss itemized deductions and the impact of state and local taxes on your federal tax bill. If you have specific questions on how the new tax bill impacts your financial or tax situation, please click here to schedule a time with Niko Finnigan, partner at Delta Wealth.