Geopolitical Conflict and Your Portfolio: What History Suggests and What to Do Now

If you’re an entrepreneur, you already know what it feels like when uncertainty spikes.

A key employee leaves unexpectedly. A vendor changes terms. A big customer delays a decision. You don’t get to vote on whether disruption happens — you only get to decide how you respond.

International conflict works the same way for markets.

The U.S.–Iran conflict is serious, and it’s normal to feel uneasy when headlines move fast. But before you make portfolio changes, it helps to step back and look at how markets have behaved around prior shocks — and, more importantly, how this recent conflict reinforces the importance of doing your homework on investments and portfolio construction.

This isn’t a prediction piece. It’s a perspective piece.

What Markets Typically Do When Conflict Breaks Out

When major geopolitical events hit, markets usually react in two phases.

Phase 1: Uncertainty hits first. Stocks can drop quickly. Volatility rises. Oil often jumps. The market is pricing future “what if's?” in real time.

Phase 2: Information replaces uncertainty. As the situation becomes clearer — even if the news is still unpleasant — markets often stabilize and re-focus on fundamentals: earnings, inflation, interest rates, and GDP growth.

That doesn’t mean “markets don’t care.” It means markets are forward-looking, and they re-price risk quickly. In fact, with this forward looking perspective, markets had already priced in a potential conflict last week.

Case Studies of International Conflict and Market Volatility

To better understand how markets respond to different international conflicts, we pulled together some recent case studies. We looked at how the stock market and oil prices responded in the days, weeks and months after the initial conflict. We wanted to examine oil prices because oil is often the transmission channel for geopolitical stress — especially when tensions involve major energy-producing regions or supply routes.

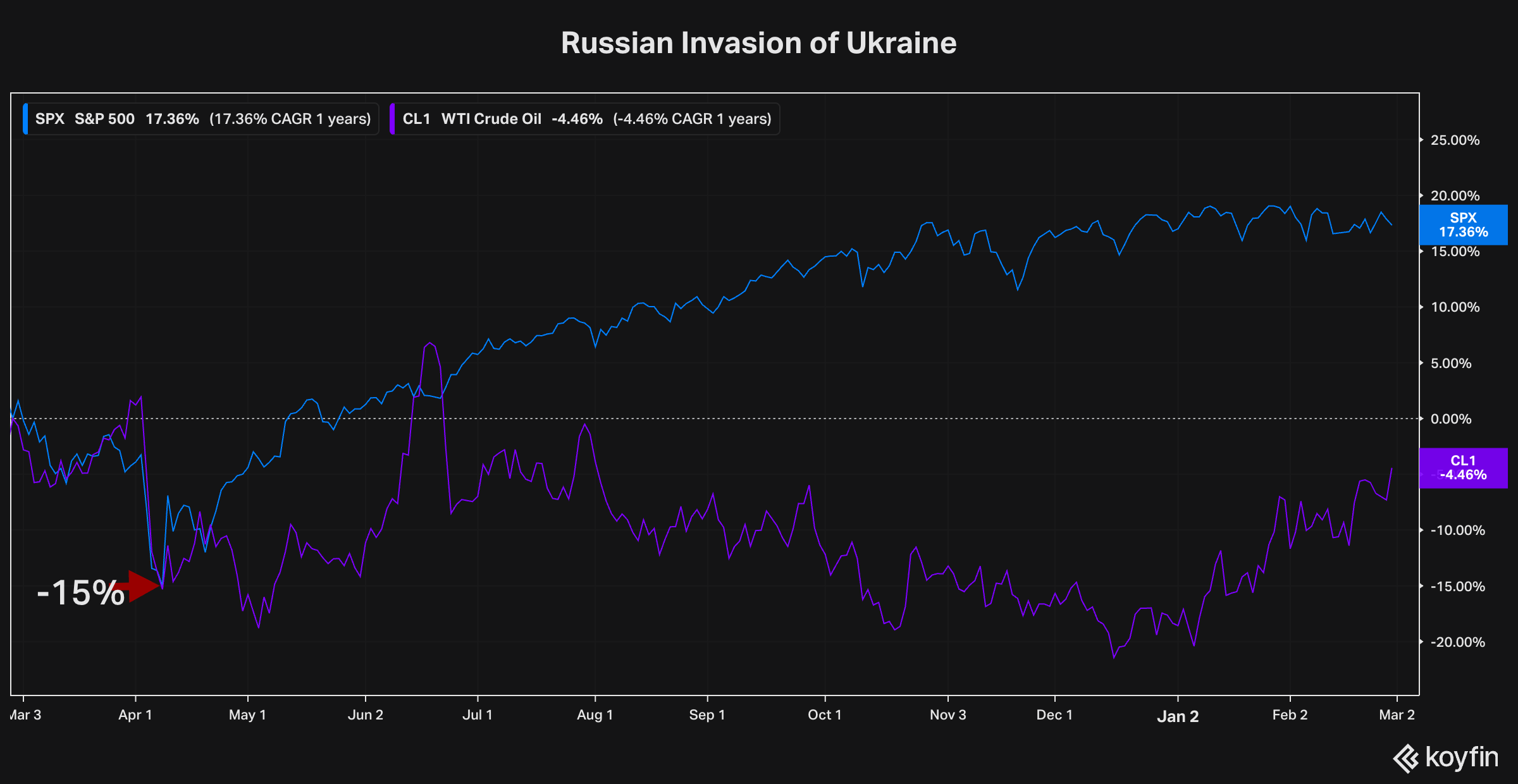

What We Can Learn From Ukraine (2022): Stocks and Oil Can Move Differently

We pulled charts around Russia’s invasion of Ukraine because it’s a clear example of how markets behave when uncertainty arrives suddenly — and how different parts of the system can respond in different ways.

One year after Russia’s invasion of Ukraine (2/24/2022)

The markets initially responded with both stocks and oil selling off--S&P 500 bottom out at a 15% loss. However, just three months after the invasion, the S&P 500 had fully recovered its losses.

One takeaway from this period is that the market can feel chaotic day-to-day, but over longer windows the driver shifts back to fundamentals.

In 2022, the invasion was a major shock. But the longer arc was shaped heavily by inflation and central bank policy. If you were only watching headlines, you would have expected one kind of market. If you were watching fundamentals, you got a clearer picture of why the market did what it did.

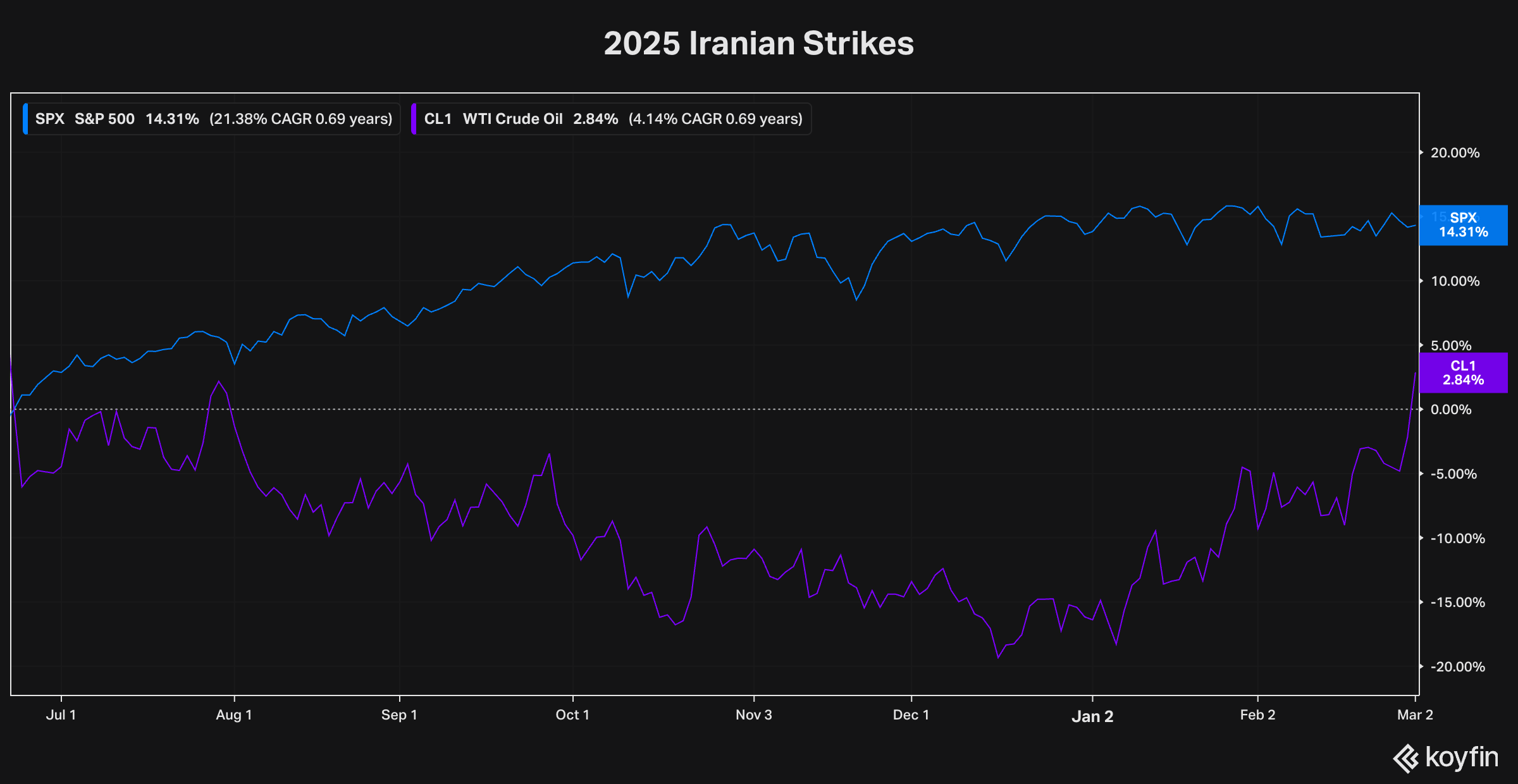

A Closer Parallel: U.S. Strikes on Iran (6/22/2025) and the Market Response

We also pulled charts around the U.S. strikes on Iran’s nuclear sites on 6/22/2025 because it’s more directly relevant to today’s U.S.–Iran conflict.

These two price movements show how markets trade more off of fundamentals than news stories. (Again, this isn't to diminish the effects of political decisions but to highlight how and why stock prices move.) The 5% loss in stocks after the Iranian strikes were dwarfed by the nearly 20% pullback that was priced in from tariff talks.

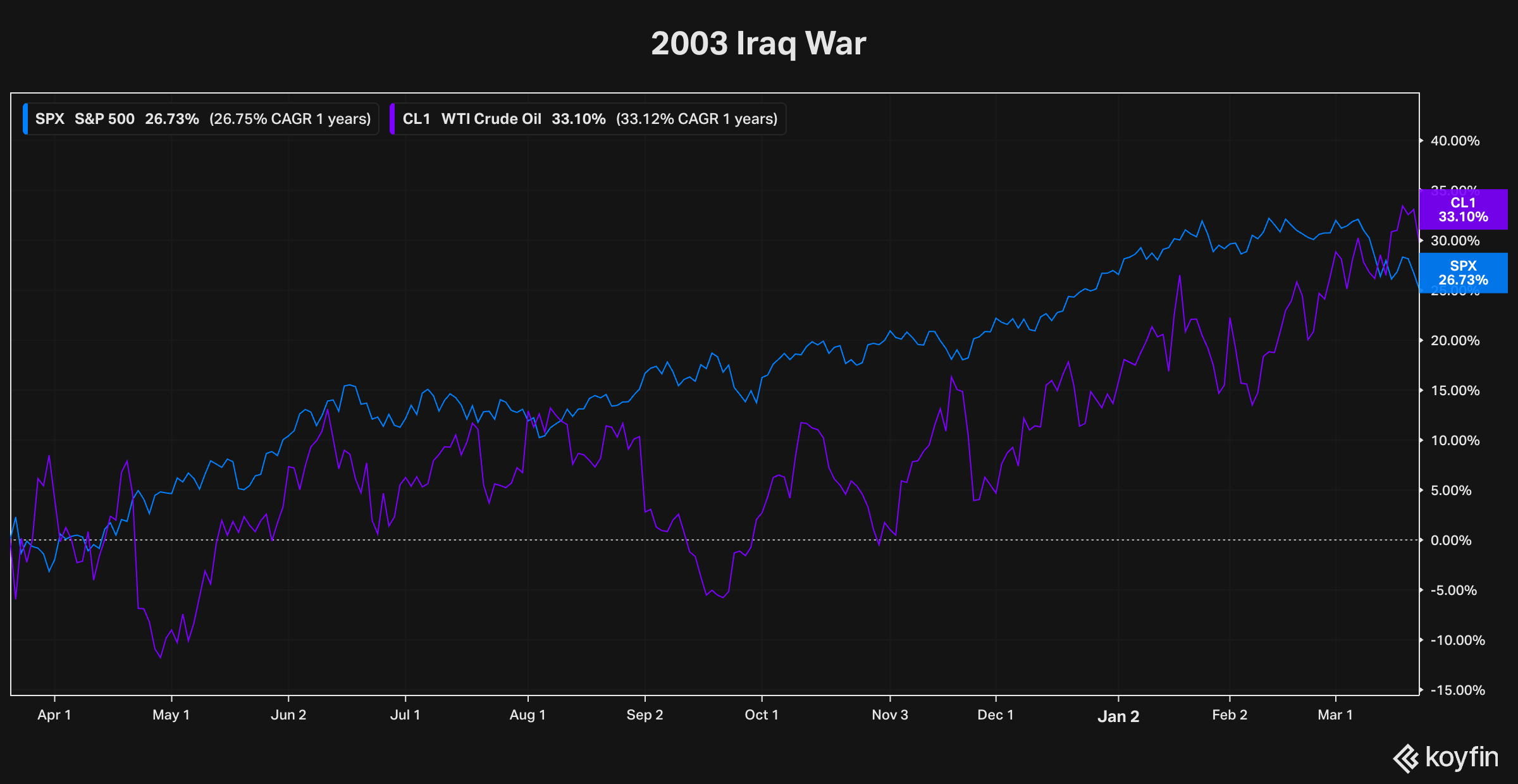

Stock and Oil Prices Rise after 2003 Iraq War

This chart matters because it shows how quickly markets can digest a shock and move on to the next question.

In this instance, both stocks and oil prices rose after the 2003 Iraq War. While this may be surprising, it highlights how capital markets can move counter to our expectations. In this scenario, stocks ultimately rose because of the expected increase in government spending from the war.

In every instance we examined, the market doesn’t just ask “What happened?” It asks:

- What’s the path from here?

- Does this change inflation?

- Does this change growth?

- Does this change interest rates?

- Does this change earnings expectations?

That’s why the best investing decisions are usually not made in the first 24–72 hours after a major headline.

What History Since 2000 Suggests About Stocks and Bonds After Major Conflicts

Looking across several major international incidents involving the U.S. since 2000, the “typical” pattern has been:

- Stocks often experience near-term volatility, then frequently recover as uncertainty fades

- High-quality bonds have often been steadier, helping to cushion portfolios during risk-off periods

In our review, the median (typical) return pattern was:

- S&P 500: +0.93% (1 week), +2.44% (1 month), +6.64% (3 months)

- U.S. bonds proxy: +0.46% (1 week), +0.29% (1 month), +1.78% (3 months)

This is not a promise about the next three months. It’s perspective: markets tend to move from “shock” to “process” faster than people expect.

The Point Isn’t to Ignore Risk — It’s to Manage It

For entrepreneurs, this is an important mindset shift.

You don’t manage business risk by trying to predict every disruption. You build systems that keep the business resilient when disruptions happen.

A portfolio should work the same way.

The goal is not to build a portfolio that “wins” in every scenario. The goal is to build a portfolio that can handle a wide range of scenarios without requiring panic moves.

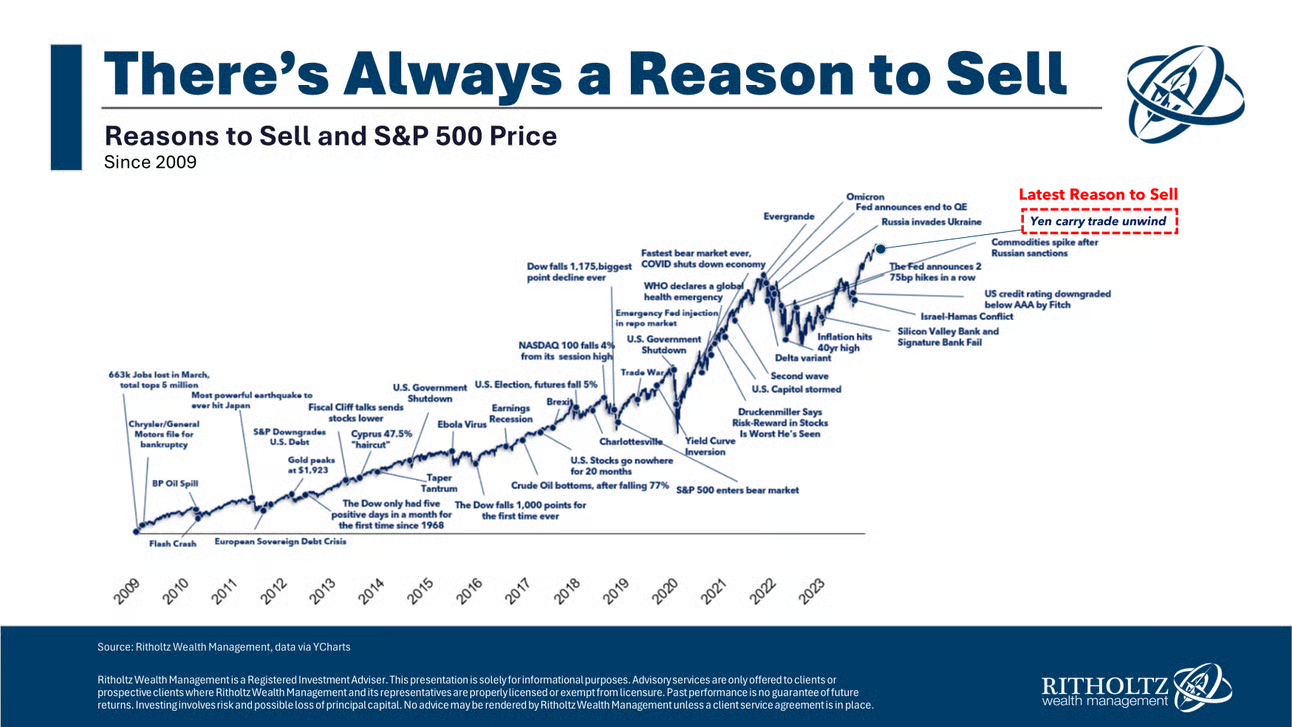

There Will Always Be a Reason to Sell

One of the most important investing lessons is also one of the most inconvenient: there will always be something to worry about.

If you look back over the last 15+ years, the market has rarely been short on reasons to “get out.” Recessions, wars, debt ceiling standoffs, bank failures, inflation spikes, pandemics — the list never ends. Yet over that same period, the market moved higher over time. The lesson isn’t that the concerns weren’t real. The lesson is that using headlines as a timing signal is a difficult game to win consistently.

This is one reason diversification matters — not just across different stocks, but across different types of assets.

Many entrepreneurs already have a form of “built-in diversification” because they hold assets that behave differently than the stock market. Real estate is a good example. It’s not perfectly stable and it’s not risk-free, but it is different. Real estate doesn’t reprice every second on your phone. That illiquidity can actually be a feature: it reduces the day-to-day noise and can make it easier to think long-term.

When part of your net worth is in assets that aren’t constantly flashing red or green, you may be less tempted to make fast decisions in the most emotional moments. For many investors, that’s the real benefit: not just diversification on paper, but diversification in behavior.

Guardrail: Real estate has its own risks (leverage, vacancies, concentration, local market risk, and liquidity constraints), so it should be sized intentionally within a broader plan rather than treated as a cure-all.

Why Moments Like This Are Stress Tests, Not Decision Points

In investing, events like the U.S.–Iran conflict are not “planning moments.” They’re “testing moments.”

A good plan is built before the test shows up.

That’s why we encourage investors (especially entrepreneurs with concentrated business risk and uneven cash flows) to treat portfolios like engineered systems:

- some components are designed to flex

- some are designed to stabilize and protect the downside

- others are designed to grow

You don’t judge the system based on one day. You judge it based on whether it behaves as expected under stress.

How We Prepare for These Moments: Stress Tests and the Metrics That Matter

The way we prepare for pop-up risk is not by guessing headlines. It’s by measuring how your portfolio is likely to behave across scenarios.

Here are three practical and objective tools we use:

Downside Capture

This is a simple question: When the market is down, how much does your portfolio typically participate in the decline?

If you’re taking 90–100% of the market’s downside, you may not be as diversified as you think. If you’re capturing a smaller portion of the downside (while still participating in long-term upside), that’s often evidence the portfolio is built to handle stress.

Scenario Analysis

Instead of debating the “next headline,” we run scenarios that have shown up repeatedly across decades:

- geopolitical events -- by using the average of prior market responses

- oil spikes and inflation shocks

- equity drawdowns (10–30%+)

- rate shocks (yields rising quickly)

- growth slowdowns / recession-style stress

A well-constructed portfolio doesn’t need to “win” every scenario. In fact, it won't. It needs to remain functional — so you can stay invested and avoid emotional decision-making.

Sortino Ratio (Risk-Adjusted Performance With a Focus on Downside)

Most people have heard of Sharpe ratio. Sharpe ratio looks at returns and market volatility, not distinguishing between upside and downside returns. Sortino is often more useful because it focuses on downside volatility — the kind of volatility that actually drives investor behavior.

When investors abandon plans, it’s usually not because the portfolio moved up. It’s because the portfolio moved down.

Sortino helps quantify whether the portfolio has historically been compensated for the downside risk it’s taking.

What to Do Right Now (Simple and Calm)

Here’s the practical guidance.

- Don’t Confuse Volatility With a Broken Plan -- volatility is normal with a portfolio built to endure it.

- Don’t Turn a Long-Term Portfolio Into a Short-Term Bet -- Big all-or-nothing moves are rarely rewarded.

- If You Feel the Urge to “Do Something,” Consider Rebalancing — Not Retreating. Rebalancing is a process-driven action. It doesn’t require predicting the future.

- Only Change Strategy If Your Reality Changed

Changes to make for the right reasons:

- your time horizon changed

- your liquidity needs changed

- your business risk changed materially

- your tax situation changed

Changes to avoid:

- “the news is scary, so we’re redesigning the plan mid-storm”

A Diversified Portfolio Is Designed for Uncertainty

If there’s one lesson history teaches investors, it’s that uncertainty isn’t a rare event. It’s a permanent feature.

That’s why a well-built portfolio assumes shocks will happen — and is designed so that shocks don’t require panic.

If you want a second opinion on how your stocks are invested — and whether your portfolio is built to behave the way you expect during periods like this — schedule a call with our Head of Wealth, Niko Finnigan, CFA. We'll walk you through how your portfolio is constructed and how we can help you navigate the market volatility.